NI 43-101 Technical Report and Preliminary Economic Assessment

Mineral Resource Estimate (“MRE”)

The MRE for the Volcan Project was prepared by Micon in accordance with the latest edition of the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by the CIM Council on May 10, 2014 (the “CIM Standards”). The tabulated mineral resources for the Volcan Project are set out in Table 1.

The mineral resources are considered as all potentially profitable blocks using the base case input parameters that are contained within the US$1,800/oz Au optimized open pit shell and below the topographic surface. The mineral resources are stated using the gold grades estimated by the Ordinary Kriging interpolation method and using capped metal grades.

The MRE is effective as of July 22, 2022. Mineral resources which are not mineral reserves do not have demonstrated economic viability.

Micon has considered the mineral resource estimates in light of known environmental, permitting, legal, title, taxation, socio-economic, marketing, political and other relevant issues and has no reason to believe at this time that the mineral resources will be materially affected by these items.

Table 1: Mineral Resource Estimate for the Volcan Project, Effective Date July 22, 2022

| Category | Tonnage (kt) |

Au Grade (g/t) |

Au Content (k. oz) |

| Measured | 123,979 | 0.700 | 2,792 |

| Indicated | 339,274 | 0.643 | 7,013 |

| M+I | 463,253 | 0.658 | 9,804 |

| Inferred | 75,018 | 0.516 | 1,246 |

Notes on the MRE:

- The updated mineral resources are reported at a cut-off grade of 0.29 g/t gold for the Dorado Oeste (DO) and Dorado Este (DE) and are reported at a cut-off of 0.75 g/t for Dorado Central.

- The effective date of the updated mineral resource estimate is July 22, 2022. Tonnages and metal content in the table are rounded to the nearest thousand, thus, numbers may not total precisely due to rounding.

- The mineral resources are reported according to the latest edition of the CIM definitions and standards which was adopted by the CIM council on May 10, 2014.

- Mineral resources which are not mineral reserves do not have demonstrated economic viability. The estimate of mineral resources may be materially affected by environmental, permitting, legal title, market conditions and other modifying factors. At the time of this report, Micon’s QPs have not been able to determine any factors that would adversely impact the current mineral resource estimate.

The updated MRE was used as a basis for a Preliminary Economic Assessment of the Project.

Preliminary Economic Assessment (“PEA”)

Tiernan initially commissioned Ausenco Chile Limitada (“Ausenco”) to compile a Preliminary Economic Assessment of the Volcan Project with an effective date of March 15, 2023, which was recently updated by Ausenco with an effective date of July 15, 2025 to take into account the following key changes:

- updated capital and operating costs data to Q1 2025;

- inclusion of the 1.5% NSR royalty sold to Franco Nevada for US$15 million in July 2023;

- updated copper and gold metal pricing to reflect current long-term consensus pricing; and

- updated Chilean tax model to reflect the new mining tax regime implemented in January 2024.

The MRE and PEA were prepared in accordance with NI 43-101. The responsibilities of the engineering companies who were contracted by Tiernan to prepare this report are as follows:

- Ausenco managed and coordinated the work related to the report, reviewed the metallurgical test results and developed PEA-level design and cost estimate for the process plant, general site infrastructure, environmental and economic analysis.

- Deswik Brazil designed the mine pit, mine production schedule, and mine capital and operating costs.

- Micon International Limited (“Micon”) completed the work related to geological setting, deposit type, exploration work, drilling, exploration works, sample preparation and analysis, data verification and developed the mineral resource estimate for the Volcan Project.

- Gestión Ambiental Consultores conducted a review of the environmental studies of the Volcan Project.

Readers are cautioned that the PEA is preliminary in nature. It includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized. Commodity prices can be volatile, and there is the potential for deviation from the forecast.

The Volcan property is located approximately 700km north of Santiago, the capital of Chile, approximately 170km by road east of the mining and agricultural city of Copiapo and approximately 40km west of the border with Argentina. The property is located in Region III of northern Chile in the Province of Copiapo and political subdivision of Comuna Tierra Amarilla.

The total area controlled comprising the Volcan Project is 45,289 hectares (ha), corresponding to the actual property boundaries. However, a title and claim search indicates that Tiernan, through its subsidiary Andina Minerals Chile SpA (“Andina Chile”), holds 55,172 ha because several areas have duplicate (overlapping) registered concessions under the various Chilean categories of mineral rights holdings. The 55,172 ha are made up of 55 mining properties, 139 exploration concessions and one exploration application owned by Andina.

Andina Chile owns water rights, which have been developed in two wells located approximately 21 km from the mineral resource area and 5 km east of the northern end corner of the Volcan concessions.

Mining Methods

The mine layout and operation are based on the following criteria:

- Two independent open-pit areas named Dorado Oeste/Central and Dorado Este, each one with a dedicated Non-Economic Rock Storage Facility

- Independent access from both pits to the mine run of mine (ROM)/crushing pad

- Low-grade stockpiling near the ROM/crushing pad

- 20m height benches

The life of mine (LOM) runs for 14 years. The basis for the scheduling includes:

- Plant feed of 60 ktpd.

- Maximum 85 Mt of material movement per year.

- Low-grade stockpiling to increase head grade for initial years.

Metallurgical Testwork

Three major phases of test work were conducted. The first consisted of initial leach, flotation tests, and comminution tests to assess the potential of the Volcan Project. This early phase of work culminated in the NI 43-101 technical report entitled “Technical Report on the Results of the Pre-Feasibility Study on the Dorado Deposits, Volcan Gold Project, Region III, Chile” dated January 31, 2011 and the last technical report filed on SEDAR+ by Andina Minerals.

This was followed by more detailed work to optimize process conditions and considerations. Andina carried out a further phase of test work in 2010, 2011 and 2012 to support a potential feasibility study for the Project.

Following its acquisition of Andina in 2012, Hochschild undertook further rounds of metallurgical testing in 2017, to develop a geometallurgical model, and in 2020, to evaluate ore sorting technology and copper flotation, and also to determine gold recovery and reagent consumption (lime and cyanide).

Recovery Methods

The plant is designed to process material at a rate of 60,000 t/d with an average head grade of 0.63 g/t of Au. The plant is designed to be operated 24 hours per day, 365 days per year.

The process plant includes the following units, processes, and facilities:

- primary crushing of ROM;

- overland conveyor system to transport coarse material;

- coarse material stockpile;

- secondary crushing and screening in closed circuit;

- tertiary crushing (HPGR);

- agglomeration and heap stacking;

- heap leach pad and ponds;

- sulphidisation, acidification, recycling, and thickening (SART) plant; and

- Adsorption, Desorption, and Recovery (ADR) - carbon-in-column (CIC), Desorption and Regeneration, and Refinery.

Environmental, Permitting and Social Considerations

The Volcan Project is in the Andean highlands area of the Atacama Region, which is characterised by extreme environmental conditions for biotic development. In this area, hyper-arid conditions, intense solar radiation, high wind speeds and daily surface freezing of watercourses constitute adverse conditions for ecosystems. Human settlements are also scarce, due to the lack of available water resources and the hostile climatic conditions during the winter, with the exception of lands used by Indigenous communities, some tourism and conservation activities.

Capital Cost Estimates

The cost estimates were developed according to the requirements for a AACE Class 5 Estimate, with an expected accuracy range of -30% to +50%.

The total initial capital cost estimate for the Volcan Project is $1,019.3m; life-of-mine sustaining capital cost is $319.5m; and the total project cost is $1,338.9m. Table 2 provides the Project cost summary for initial and sustaining capital cost.

Table 2: Summary of Capital Costs (all figures are in US$ million)

| Description | Initial Capital | Sustaining Capital | Total Capital |

| Mining | 82.8 | 18.7 | 101.4 |

| Process | 372.3 | 168.9 | 541.2 |

| Infrastructure – On site | 65.0 | - | 65.0 |

| Infrastructure – Off site | 88.5 | - | 88.5 |

| Total Direct (US$m) | 608.6 | 187.6 | 796.2 |

| Project Indirect Cost | 161.4 | 60.5 | 221.8 |

| Owner Cost | 43.7 | 15.2 | 58.9 |

| Contingency | 205.6 | 56.3 | 261.9 |

| Total Capex Class 5 (US$m) | 1,019.3 | 319.5 | 1,338.9 |

Operating Cost Estimates

A summary of the individual components that make up the LOM operating costs is presented in Table 3. Mine operating cost weighted averages are indicated separately for the Years 1-10 which correspond to the active mining period and Years 11-14 which corresponds to low grade stockpile rehandle only.

Table 3: Summary of Operating Cost Estimate

| Area | Units | Avg. Y 1 – Y10 Mining |

Avg. Y11 – Y14 Stockpile Rehandle Only |

Avg. LOM |

| Mining | US$/t moved | 2.10 | 0.73 | 1.94 |

| Mining | US$/t processed | 7.14 | 0.73 | 5.44 |

| Processing | US$/t processed | 6.77 | 6.75 | 6.76 |

| G&A | US$/t processed | 1.09 | 0.66 | 0.97 |

| Total Operating Cost | US$/t processed | 15.00 | 8.14 | 13.17 |

Economic Analysis

The economic analysis was performed assuming an 5% discount rate. Cash flows have been discounted to the beginning of construction on January 1, 2030, assuming that the Project execution decision will be made and major project financing will be carried out at this time.

The pre-tax net present value (“NPV”) discounted at 5% (NPV5%) is US$2.5 billion, the internal rate of return (“IRR”) is 36.6%, and payback is 2.3 years. On an after-tax basis, the NPV5% is US$1.5 billion, the IRR is 28.7%, and the payback period is 2.6 years. A summary of the Project economics is included in Table 4.

Table 4: Economic Analysis Summary

| General | LOM Total / Avg |

| Gold Price (US$/oz) | 2,400 |

| Mine Life (years) | 13.6 |

| Production | LOM Total / Avg |

| Total Plant Feed Tonnes (kt) | 293,165 |

| Plant Feed Head Grade Au (g/t) | 0.63 |

| Leach Recovery Rate Au (%) | 64.2% |

| Total Gold Ounces Recovered (koz) | 3,820 |

| Total Average Annual Gold Production (koz) | 281 |

| Average Year 1 to 10 Annual Gold Production (koz) | 332 |

| Operating Costs | LOM Total / Avg |

| Total Operating Costs (US$/t Processed) | 13.2 |

| Cash Costs* (U$/oz Au) | 1,002 |

| AISC** (US$/oz Au) | 1,094 |

| Capital Costs | LOM Total / Avg |

| Initial Capital (US$m) | 1,019 |

| Sustaining Capital (US$m) | 320 |

| Closure Costs (U$m) | 30 |

| Financials - Pre-Tax | LOM Total / Avg |

| NPV (5%) (US$m) | 2,470 |

| IRR (%) | 36.6% |

| Payback (years) | 2.3 |

| Financials - Post-Tax | LOM Total Avg |

| NPV (5%) (US$m) | $1,513 |

| IRR (%) | 28.7% |

| Payback (years) | 2.6 |

* Cash costs consist of mining costs, processing costs, mine-level G&A, copper revenue credit, refining charges and royalties over payable gold ounces

** AISC includes cash costs plus sustaining capital and closure cost over payable gold ounces

Sensitivity Analysis

A sensitivity analysis was conducted on the base case pre-tax and after-tax NPV, IRR, and payback of the Project, using the following variables: metal price, discount rate, leach recovery, initial capital costs, and operating costs. Analysis revealed that the Project is most sensitive to changes in metal price, leach recovery, then, to a lesser extent, to operating costs and initial capital costs.

Table 5 and Table 6 presents a summary of the Sensitivity Analysis.

Table 5: Sensitivity Analysis Pre-Tax Summary (all figures are US$ million, except gold price which is US$/ounce)

| Gold Price | Base Case | Total Capex | Total Opex | |||

| NPV (5%) | IRR | -25% | 25% | -25% | 25% | |

| $1,800 | $916 | 18.5% | $1,219 | $613 | $1,574 | $258 |

| $2,400 | $2,470 | 36.6% | $2,773 | $2,167 | $3,128 | $1,812 |

| $3,000 | $4,024 | 52.6% | $4,327 | $3,721 | $4,683 | $3,366 |

| $3,600 | $5,579 | 67.3% | $5,881 | $5,276 | $6,237 | $4,920 |

Table 6: Sensitivity Analysis Post-Tax Summary (all figures are US$ million, except gold price which is US$/ounce)

| Gold Price | Base Case | Total Capex | Total Opex | |||

| NPV(5%) | IRR | -25% | 25% | -25% | 25% | |

| $1,800 | $531 | 14.3% | $748 | $315 | $947 | $93 |

| $2,400 | $1,513 | 28.7% | $1,658 | $1,302 | $1,932 | $1,128 |

| $3,000 | $2,357 | 38.2% | $2,513 | $2,289 | $2,780 | $2,020 |

| $3,600 | $3,246 | 47.0% | $3,382 | $3,119 | $3,638 | $2,854 |

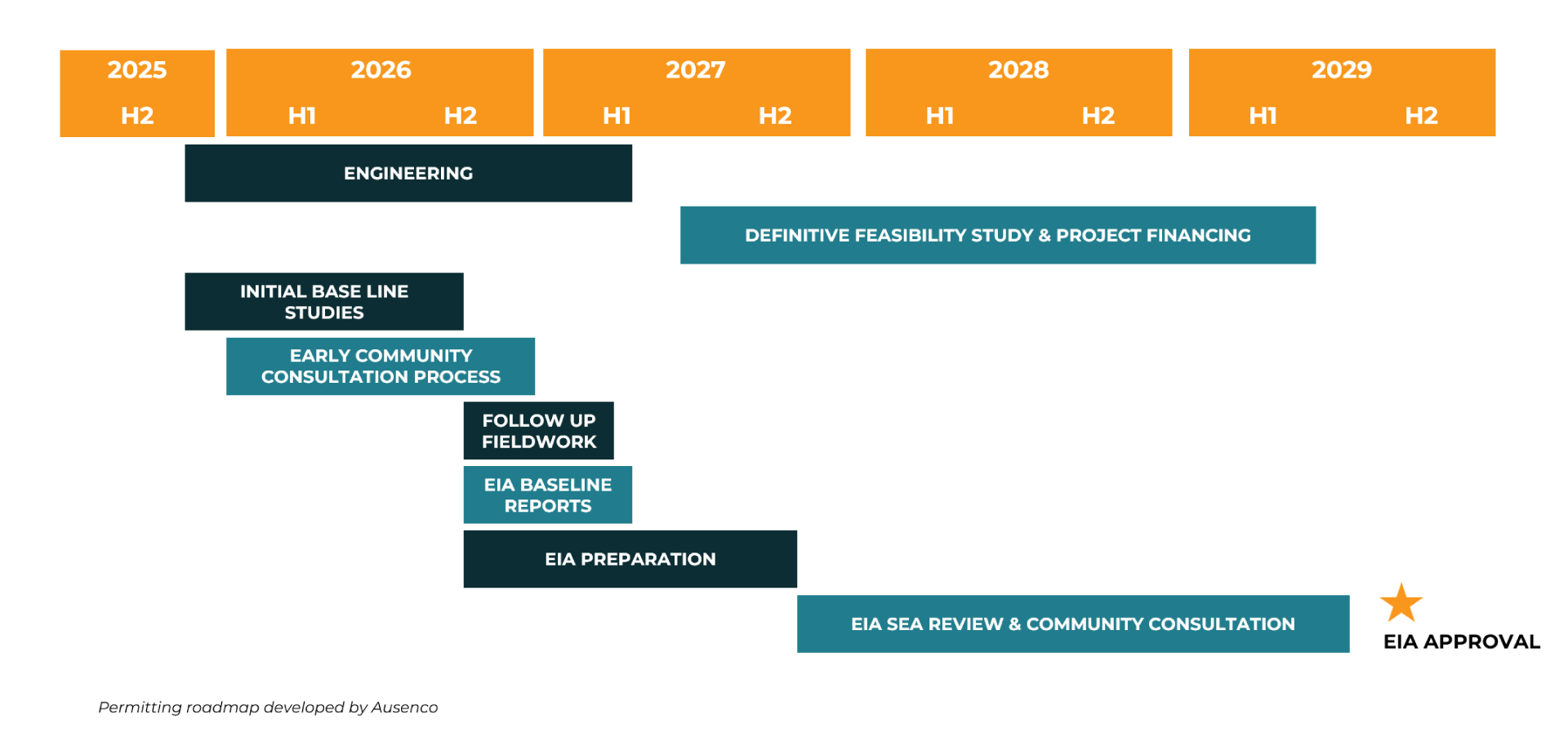

Permitting Roadmap

PEA Interpretations and Conclusions

Based on the assumptions and parameters presented, the PEA shows positive economics (i.e. US$1.5 billion post-tax NPV (5%) and 28.7% post-tax IRR). The PEA supports a decision to carry out additional detailed studies.

Preliminary Economic Assessment Report

1For further information, refer to the technical report entitled “Volcan Project – NI 43-101 Technical Report on Preliminary Economic Assessment” dated August 29, 2025 with an effective date of July 15, 2025 as prepared by Ausenco. The technical report can be found on the website of Tiernan Gold at www.tiernangold.com.

2All-in-Sustaining Costs are defined as Cash Costs plus sustaining capital and closure costs over payable gold ounces.